If you heard that Thailand charges a flat 15% cryptocurrency tax on your profits, stop right there. That information is outdated and likely to cost you money if you act on it blindly. As of May 2026, the landscape for digital assets in Thailand has shifted dramatically. Instead of a high capital gains tax for most residents, the country is currently running a major incentive program designed to attract global attention.

The reality is much more favorable than the old rumors suggest. Through a specific window ending in 2029, personal income tax on cryptocurrency capital gains is effectively zero-if you follow strict rules. This isn't just a loophole; it's a deliberate national strategy. But there are traps. If you trade on the wrong platform or earn money through staking, that 'zero tax' promise vanishes instantly. Let’s break down exactly how this works so you don’t accidentally trigger a tax bill from the Revenue Department.

The Big Shift: From 35% to 0% Capital Gains

To understand why the current rules matter, you have to look at what changed. Before September 2025, selling Bitcoin or Ethereum in Thailand was expensive. Your profits were added to your total annual income and taxed at progressive rates that could reach up to 35%. For companies, corporate tax hovered around 20%. It was a heavy burden that pushed many traders toward offshore platforms where regulations were looser.

Then came Ministerial Regulation No. 399 (B.E. 2568). Published in the Royal Gazette on September 5, 2025, this regulation introduced a five-year personal income tax exemption on cryptocurrency capital gains. It runs from January 1, 2025, through December 31, 2029. The Cabinet approved this move on June 17, 2025, with Deputy Minister of Finance Julapun Amornvivat calling it a key step to boost Thailand’s economic potential.

The goal? To make Thailand a premier "Digital Asset Hub." By removing the tax penalty on trading profits, the government hopes to stimulate market activity, attract foreign investment, and keep transactions within its own regulated ecosystem. They project this will generate about $1 billion annually in indirect revenue through increased spending and investment, even though they aren't taxing the gains directly.

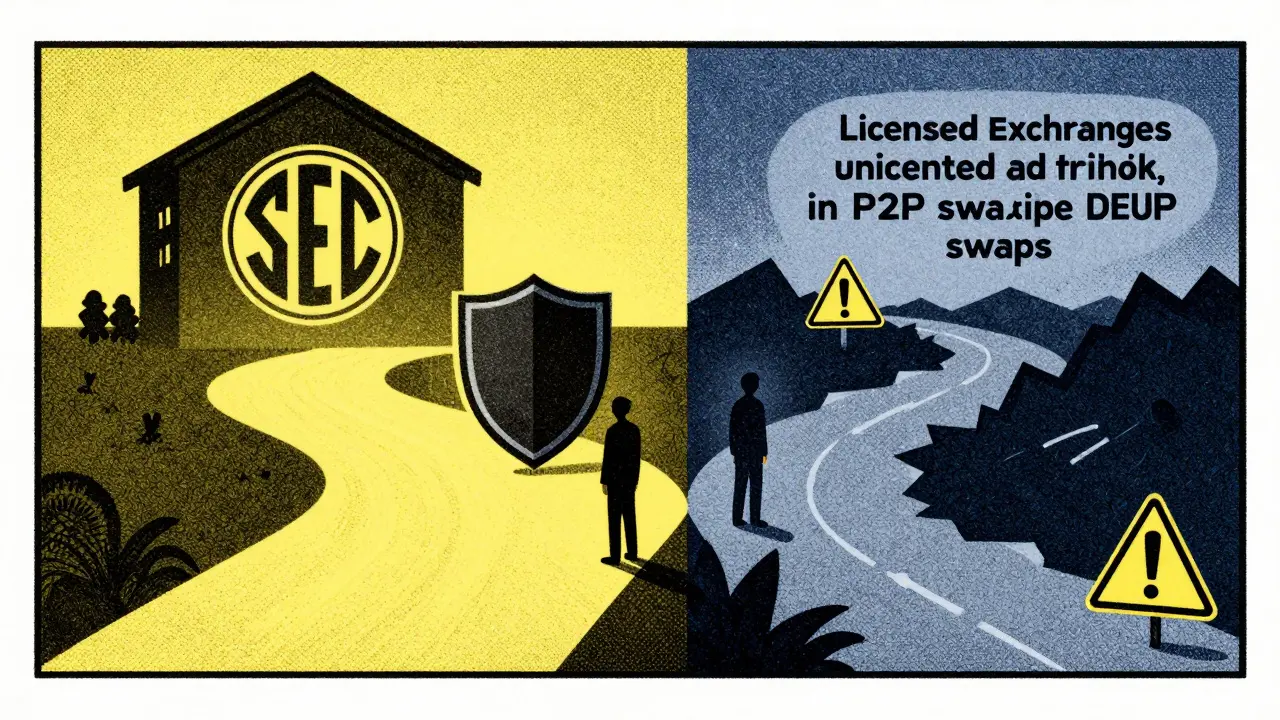

The Golden Rule: Only Licensed Platforms Count

This is where most people get confused. The tax exemption is not universal. It does not apply to every transaction you make with crypto. It applies strictly to profits from sales or transfers conducted through digital asset exchanges, brokers, or dealers that are licensed by the Thai Securities and Exchange Commission (SEC).

You need to verify your exchange. If you are using a platform that holds a license under the 2018 Digital Asset Business Decree, your capital gains are exempt. If you are using an international exchange that does not have a Thai license, those profits are taxable. The Thai Revenue Department categorizes cryptocurrencies as "digital assets," but the source of the transaction determines the tax treatment.

Why such a strict rule? The government wants to build a domestic crypto ecosystem. They want you to trade locally, where they can monitor compliance and ensure consumer protection. Using unlicensed platforms bypasses this safety net, and the tax exemption is the carrot used to pull you back into the regulated system.

| Activity Type | Platform/Method | Tax Status |

|---|---|---|

| Capital Gains (Trading) | Thai SEC-Licensed Exchange | Exempt (0%) |

| Capital Gains (Trading) | Unlicensed/International Exchange | Taxable (Up to 35%) |

| P2P / DeFi Swaps | Decentralized (DEX) or Direct Transfer | Taxable |

| Staking Rewards | Any Platform | Taxable (Ordinary Income) |

| Mining Rewards | Any Platform | Taxable (Ordinary Income) |

| Lending/Yield Interest | Any Platform | Taxable |

What Is Actually Taxable?

Even with the exemption, you are not free from all taxes. The exemption only covers "capital gains" from buying low and selling high on licensed exchanges. Several other common crypto activities remain fully taxable.

First, decentralized finance (DeFi) is out. If you swap tokens on a decentralized exchange (DEX) like Uniswap, or engage in peer-to-peer (P2P) sales directly between wallets, those profits are not covered by the exemption. The Thai SEC cannot regulate these off-platform transactions, so the Revenue Department treats them as standard taxable income.

Second, passive income is taxable. Staking rewards, mining earnings, and interest from crypto lending platforms are considered ordinary income. They are not capital gains. You must report these amounts on your tax return, and they will be taxed according to your regular income tax brackets. There is no special exemption for yield farming or staking yet.

Third, derivatives are excluded. Profits from futures, options, or other digital asset derivatives do not qualify for the capital gains exemption. These complex instruments are treated differently because of their speculative nature and leverage risks.

The Real Source of the "15%" Myth

So where did the idea of a 15% crypto tax come from? It is real, but it applies to a different group of people. Thailand imposes a 15% withholding tax on crypto income earned by foreign entities.

If you are a non-resident entity earning cryptocurrency income sourced from Thailand, this withholding tax applies. It is a separate mechanism from the domestic capital gains rules. For Thai residents and individuals living in Thailand who are tax residents, this 15% rate does not apply to their personal trading gains-provided they use licensed exchanges. Confusing these two rules leads to unnecessary panic and incorrect financial planning.

How to Stay Compliant in 2026

Compliance is not automatic. Just because the tax is exempt doesn't mean you ignore your records. The Thai Revenue Department requires detailed documentation to prove that your trades occurred on licensed platforms.

Here is your checklist for staying safe:

- Verify Your Exchange: Check the Thai SEC website regularly to ensure your exchange maintains its license. Licenses can be revoked.

- Separate Wallets: Keep your trading activity on licensed exchanges distinct from your DeFi or P2P activities. Mixing them makes reporting difficult.

- Track All Transactions: Use accounting software that can import data from your exchange. You need to show the date, amount, price, and platform for every trade.

- Report Passive Income: Do not forget to declare staking or mining rewards. These are not exempt, and missing them can lead to penalties.

- File Annually: Even if your gain is zero due to the exemption, you may still need to file a return to demonstrate compliance, depending on your overall income level.

The principle is simple: the exemption is a privilege granted for participating in the regulated market. If you step outside that market, you lose the privilege.

Looking Beyond 2029

This tax holiday ends on December 31, 2029. After that, the government will reassess the framework. Will they extend it? Modify it? Or return to previous rates? Nobody knows for sure yet. However, the Ministry of Finance is monitoring metrics closely. If the goal of generating $1 billion in annual economic activity is met, there is a strong argument for continuing some form of favorable treatment.

For now, 2026 is a prime year to take advantage of this policy. Long-term investors should consider consolidating their trading onto Thai-licensed platforms to maximize tax efficiency during this window. Short-term traders should avoid DeFi and P2P markets if tax minimization is their priority.

Thailand is positioning itself as a leader in Southeast Asia’s crypto landscape. By offering clarity and incentives, they are attracting entrepreneurs and investors. But with great opportunity comes great responsibility. Understanding the difference between a licensed trade and an unregulated one is the single most important factor in your tax outcome.

Is cryptocurrency trading legal in Thailand?

Yes, cryptocurrency trading is legal in Thailand, provided it is conducted through platforms licensed by the Thai Securities and Exchange Commission (SEC). Trading on unlicensed platforms is risky and may result in taxable events without regulatory protection.

Do I pay tax on crypto gains in Thailand in 2026?

If you are a Thai tax resident and trade on a Thai SEC-licensed exchange, your capital gains are exempt from personal income tax until December 31, 2029. If you trade on unlicensed platforms or engage in DeFi/P2P, your gains are taxable.

What is the 15% crypto tax in Thailand?

The 15% figure refers to a withholding tax applied to cryptocurrency income earned by foreign entities (non-residents). It does not apply to Thai residents' personal capital gains from licensed exchanges.

Are staking rewards taxable in Thailand?

Yes, staking rewards, mining income, and lending yields are considered ordinary income and are fully taxable. They are not covered by the capital gains exemption.

When does the crypto tax exemption end?

The current five-year exemption period for personal capital gains on licensed exchanges ends on December 31, 2029. Future policies after this date are subject to government review.