Imagine buying a slice of a Manhattan apartment or a vacation home in the Alps with a few clicks on your phone. It sounds like the future, but right now, it’s a legal minefield. Real estate NFTs are digital tokens on a blockchain that represent ownership or rights to physical properties. While the technology is ready, the laws governing them are still catching up.

You might think holding an NFT means you own the building. In most places, that’s not true. The biggest hurdle isn’t the code; it’s the courtroom. If you’re looking to invest or tokenize property in 2026, you need to understand how these digital certificates interact with centuries-old property laws. This guide breaks down the actual rules, the risks, and where things stand globally so you don’t lose money-or face legal trouble.

The Core Problem: Digital Tokens vs. Physical Deeds

The fundamental issue with property tokenization is the disconnect between the blockchain and the government registry. When you buy a house traditionally, you sign papers, pay taxes, and record the deed at a county office. With an NFT, you get a cryptographic token. But does that token give you the right to live in the house? Can you evict a tenant? Usually, no.

In 2023, the Law Commission of England and Wales published a major consultation paper stating that crypto tokens should be recognized as personal property under English law. They argued that digital assets have more in common with physical objects than with traditional intangible rights. However, they made a crucial distinction: owning the NFT is not the same as owning the real-world asset it represents. The NFT is just a receipt, not the title itself.

This creates a dangerous gap. In a high-profile case in Miami, a buyer purchased a penthouse for $654,000 via an NFT platform. The transaction went through on-chain, but because the traditional deed wasn’t properly recorded with the county, the buyer didn’t legally own the property. The NFT proved they paid, but it didn’t prove they owned. This "legal fiction"-where the blockchain says one thing and the law says another-is the primary risk for investors today.

How It Actually Works: The SPV Structure

To bridge this gap, most legitimate projects use a specific legal structure called a Special Purpose Vehicle (SPV). Here’s how it works in practice:

- Create an LLC: A lawyer sets up a Limited Liability Company (LLC) specifically to hold the title to the physical property. This is often done in Delaware, USA, because its corporate laws are flexible and well-established.

- Tokenize Membership: Instead of selling the house directly, the company sells membership interests in the LLC. These interests are represented by NFTs or security tokens on a blockchain like Ethereum or Polygon.

- Link On-Chain to Off-Chain: The smart contract governing the NFT references the LLC’s operating agreement. This agreement states that whoever holds the token is entitled to the profits and voting rights of the LLC.

According to LegalNodes’ 2024 analysis of 47 tokenized real estate projects, 89% used this Delaware LLC model for U.S. properties. This structure keeps the physical deed safe in traditional records while allowing fractional ownership to trade digitally. However, it adds complexity. You aren’t buying the house; you’re buying a share of a company that owns the house. This distinction matters heavily for tax purposes and investor rights.

Securities Law: The SEC’s Red Line

If you’re in the United States, the biggest regulatory hurdle isn’t property law-it’s securities law. The Securities and Exchange Commission (SEC) looks closely at whether your NFT is a "security." Under the Howey Test, if people invest money expecting profits from the efforts of others, it’s a security.

For real estate, this almost always applies. If your NFT promises rental income or profit from property appreciation, the SEC considers it a security. This means you must comply with strict regulations:

- Regulation D (Rule 506c): You can only sell to accredited investors (high-net-worth individuals). You must verify their status and file Form D with the SEC.

- Regulation A+: Allows broader sales to the public but requires extensive disclosure documents and SEC review, costing tens of thousands of dollars.

The SEC has been aggressive here. Between 2021 and 2024, they filed 17 enforcement actions against non-compliant real estate tokenization projects. In 2023, the SEC sued the REcoin Foundation, establishing that any expectation of profit from property management triggers securities classification. Even "utility" NFTs that only grant access rights (like using a vacation home) face scrutiny if there’s any hint of investment return. Ignoring this doesn’t just mean fines; it can lead to criminal charges for fraud.

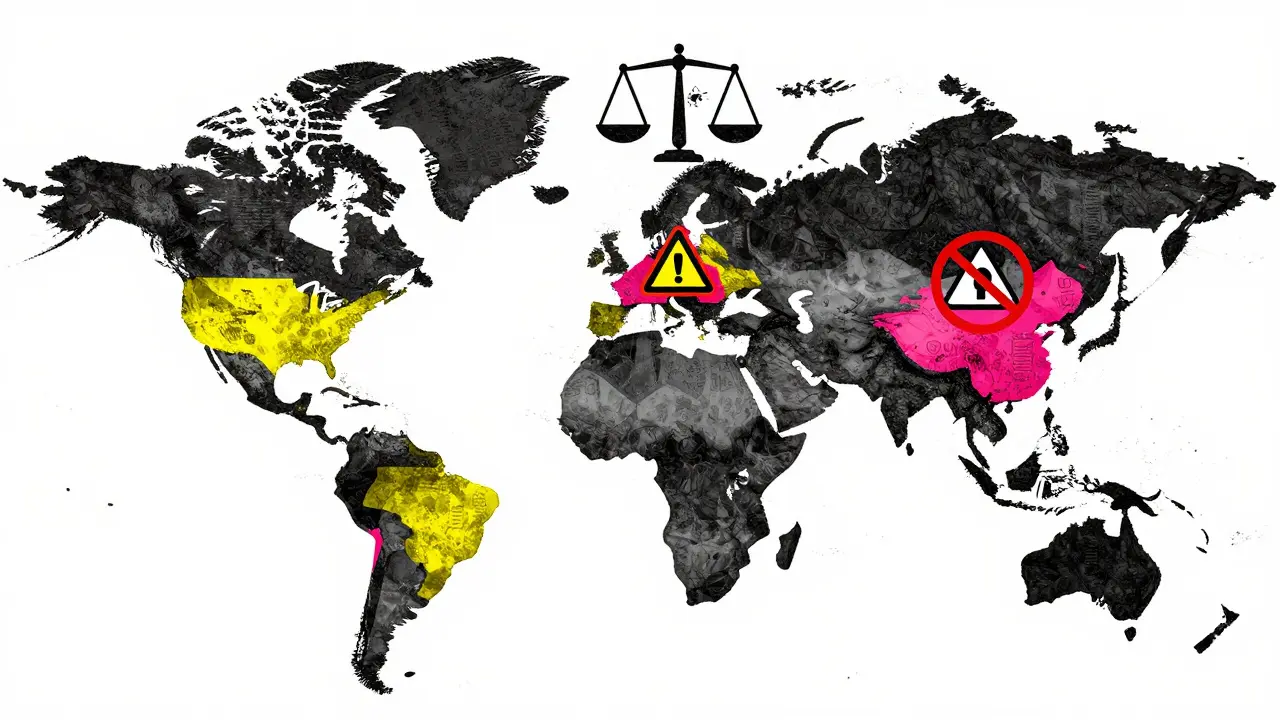

Global Regulatory Landscape: Where Can You Play?

Property law is territorial, but blockchains are global. This mismatch creates wild differences depending on where you and the property are located. Here’s how key jurisdictions handle blockchain deeds as of 2026:

| Jurisdiction | Legal Status of NFTs | Key Requirements | Risk Level |

|---|---|---|---|

| United States | Varies by state; mostly treated as securities | SEC compliance (Reg D/A+), KYC/AML, SPV structure | High (due to fragmentation) |

| Wyoming, USA | Recognizes blockchain-based property records | NFT deeds must link to county records via QR code | Low (for local properties) |

| Switzerland | Recognized as securities if profit-sharing | FINMA guidelines, listing on SIX Digital Exchange | Medium (clear rules) |

| UAE (Dubai) | Fully regulated exchange approved | SCA approval, licensed platforms only | Low (innovative framework) |

| China | Prohibited | No NFTs representing real-world assets allowed | Critical (illegal) |

Switzerland and the UAE have moved fast. Dubai launched the world’s first fully regulated real estate NFT exchange in 2023, allowing 127 properties to be tokenized by late 2024. Switzerland’s FINMA provides clear guidelines, treating profit-sharing NFTs as securities that must trade on licensed exchanges. In contrast, China banned all NFTs representing real-world assets in 2022, making any such transaction illegal despite heavy blockchain development activity.

In the U.S., only three states-Wyoming, Vermont, and Ohio-have enacted specific legislation recognizing blockchain-based property records. Wyoming’s 2025 update requires NFT-based deeds to include a QR code linking to the county’s traditional records system, a hybrid approach adopted by eight other states by mid-2025. Everywhere else, you’re relying on private contracts, which are harder to enforce.

Tax Implications: It’s Not Just Capital Gains

Taxes are where many investors get burned. Because the legal nature of real estate NFTs is ambiguous, tax authorities often treat them inconsistently. In the U.S., the IRS generally views crypto transactions as taxable events. Every time you buy, sell, or swap an NFT, you may trigger capital gains tax.

But it gets messier with rental income. If your NFT represents a share in an LLC that owns a rental property, the IRS may view the distributions as ordinary income, not capital gains. This means higher tax rates. Furthermore, 34% of users in a 2025 survey reported tax complications due to inconsistent state treatment of crypto dividends. Some states tax crypto transfers as sales tax events, while others ignore them until fiat conversion.

International investors face double taxation risks. If you’re a U.S. citizen buying a tokenized property in Dubai, you owe taxes to both the UAE (if applicable) and the IRS. The lack of standardized international treaties for digital assets means you often have to navigate this alone, hiring expensive cross-border tax attorneys.

Practical Steps to Stay Compliant

If you’re serious about entering this space, don’t just mint a token and hope for the best. Follow these steps to mitigate legal risk:

- Choose the Right Jurisdiction: For U.S. properties, consider Wyoming or Delaware for the SPV. Avoid states with unclear blockchain laws. For international deals, prioritize UAE or Switzerland for clearer frameworks.

- Use a Legal Wrapper: Never tokenize a property directly without an underlying legal entity (LLC/SPV). Ensure the operating agreement explicitly links token ownership to economic rights.

- Conduct Full KYC/AML: Implement identity verification that meets FATF Travel Rule requirements. This costs $8,000-$12,000 but protects you from money laundering charges.

- Audit Smart Contracts: Hire firms like Quantstamp or OpenZeppelin to audit your code. A bug in the contract can lead to lost funds or unauthorized transfers, creating massive liability.

- Disclose Securities Status: If there’s any profit expectation, register as a security or use an exemption. File Form D with the SEC if using Reg D. Transparency prevents enforcement actions.

The average legal compliance cost for tokenizing a $1 million property is around $47,300-18% higher than traditional securitization. But this cost buys you protection. Projects that skip these steps fail at a rate of 22%, according to CRE Finance Council data from 2024.

Future Outlook: What’s Coming in 2026 and Beyond

The landscape is shifting rapidly. In December 2024, the CFTC and SEC jointly proposed rules requiring all real estate NFT platforms to register as Alternative Trading Systems. This would bring institutional-grade oversight to the market. Meanwhile, the European Union’s MiCA II framework, expected to pass in Q3 2025, will establish EU-wide standards for real-world asset tokenization, including mandatory integration with national title registries.

Institutional interest is growing. BlackRock launched its Blockchain Real Estate Fund in January 2025, requiring dual on-chain/off-chain title verification for all assets. By 2027, 73% of REITs plan to allocate 5-15% of new acquisitions to tokenized assets. The World Economic Forum predicts 10% of global real estate will be tokenized by 2030, provided three gaps are closed: standardized cross-jurisdictional registry integration, clear tax frameworks, and international dispute resolution mechanisms.

Until then, proceed with caution. The technology is promising, but the law is still writing the rules. Protect yourself by understanding the difference between holding a token and holding a deed.

Is owning a real estate NFT the same as owning the property?

No. In most jurisdictions, an NFT is a digital certificate that represents a contractual right or membership interest in a company (SPV) that owns the property. It does not automatically transfer the legal title of the physical asset unless the local government explicitly recognizes blockchain deeds, which is rare outside of specific states like Wyoming.

Are real estate NFTs considered securities in the US?

Yes, if they offer profit participation. The SEC treats most real estate NFTs as securities under the Howey Test because investors expect profits from the management or appreciation of the property. This requires compliance with federal securities laws, such as Regulation D or A+, and limits sales to accredited investors unless full registration is obtained.

What happens if I buy a real estate NFT in a country where it's illegal?

You risk losing your entire investment and facing legal penalties. For example, China bans NFTs representing real-world assets. Transactions involving residents of such countries are void and unenforceable. Always check local regulations before participating in any tokenization project.

How do I ensure my real estate NFT project is compliant?

Start by forming an SPV (like a Delaware LLC) to hold the property title. Use a legal wrapper that links token ownership to LLC membership. Conduct thorough KYC/AML checks, audit your smart contracts, and consult with securities lawyers to determine if you need to file with the SEC or other regulators.

Which countries have the best legal frameworks for real estate NFTs?

As of 2026, the UAE (specifically Dubai) and Switzerland lead with clear regulations and licensed exchanges. In the US, Wyoming offers the most supportive state-level laws for blockchain deeds. These jurisdictions provide clarity on securities status and property recognition, reducing legal risk for investors.