Imagine walking into your local bank branch to withdraw cash, only to be told that physical bills are becoming obsolete. Instead, you check an app linked directly to the central bank, where your money sits in a digital wallet with zero risk of bank failure. This isn’t science fiction anymore. It’s the reality unfolding with Central Bank Digital Currencies (CBDCs), which are digital forms of national fiat currencies issued directly by central banks.

As of 2024, 134 countries representing 98% of global economic output are actively researching or preparing to launch their own digital currencies. China and the Bahamas have already launched operational systems. The question is no longer *if* CBDCs will arrive, but how they will reshape the $120 trillion global banking industry. For traditional banks, this shift poses an existential threat wrapped in a technological upgrade.

The Core Threat: Disintermediation of Banks

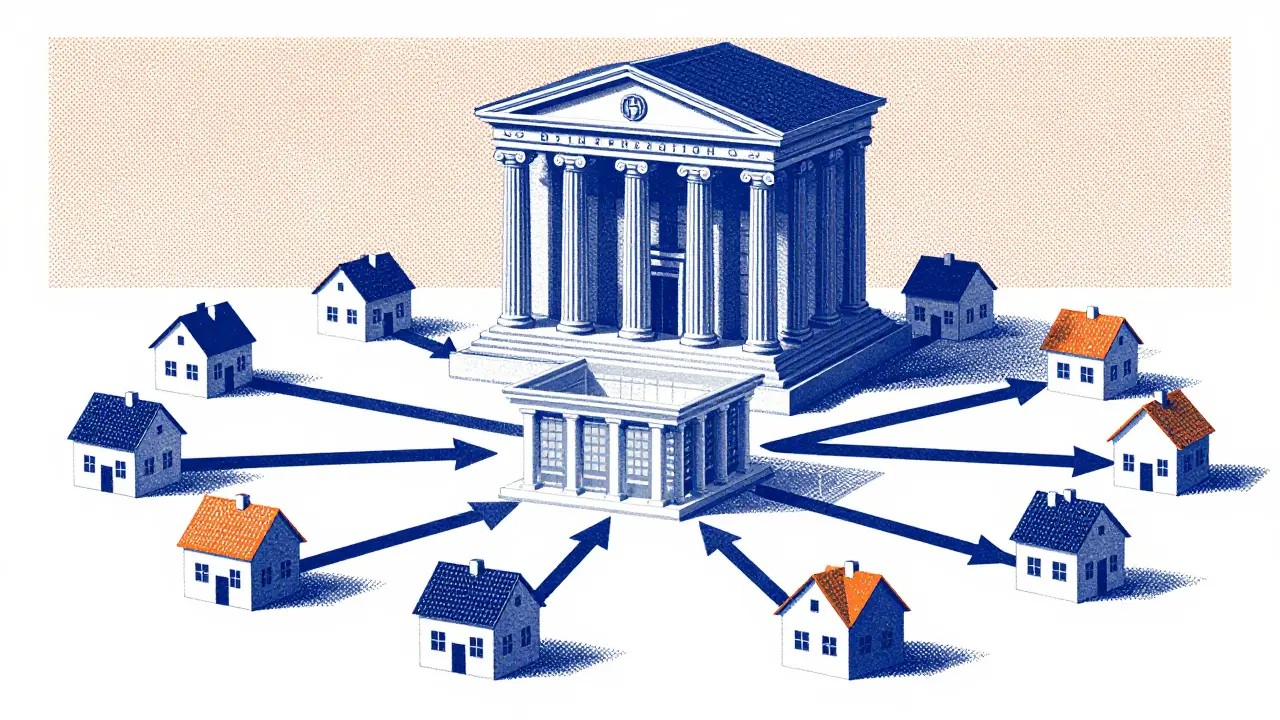

The biggest fear for traditional bankers is disintermediation. In simple terms, this means customers bypassing commercial banks entirely to hold money directly at the central bank. Historically, you deposited money in a bank, and the bank lent it out to businesses and homeowners. The bank took the risk; you got safety and interest.

With a CBDC, the central bank becomes the direct provider of retail deposits. According to research from the Bank for International Settlements (BIS), this creates two dangerous scenarios for traditional banks:

- Slow Disintermediation: During normal times, people move some savings to CBDCs because they offer a safe, government-backed alternative. This raises funding costs for banks as they compete for remaining deposits.

- Fast Disintermediation: During a banking crisis, panic sets in. If users can instantly move funds from a struggling commercial bank to a risk-free CBDC account, bank runs could happen in seconds rather than days.

Data from a German household survey highlights this risk. When asked about a hypothetical digital euro, 67% of respondents said they would replace some bank deposits with CBDC during normal times. But during simulated banking stress, that number jumped to 82%. Without safeguards, this mass exodus could destabilize the entire financial system.

| Feature | Traditional Bank Deposit | CBDC Holding |

|---|---|---|

| Risk Level | Low (insured up to limits) | Zero (direct central bank liability) |

| Interest Rates | Variable, set by bank | Set by central bank policy |

| Privacy | Moderate (bank knows your data) | Low (central bank tracks transactions) |

| Lending Role | Bank uses deposits to lend | No lending function; pure payment tool |

| Accessibility | Requires bank account | Direct access via digital wallet |

Profitability Squeeze: What Happens to Lending?

Banks don’t just store money; they create credit. They take deposits and lend them out to fuel business growth, home purchases, and consumer spending. If deposits flee to CBDCs, banks have less capital to lend. A general equilibrium model developed by researchers at the Centre for Economic Policy Research (CEPR) shows that CBDC adoption could reduce bank profitability by 12-15% and decrease lending to businesses by 8-10%.

This matters because reduced lending leads to lower investment and slower economic production. While households benefit from secure savings options and potentially higher deposit rates (an average 0.35 percentage point increase in competitive markets), the broader economy might suffer if credit dries up. The trade-off is clear: greater safety for savers versus potential stagnation for borrowers.

To mitigate this, experts suggest implementing holding limits. The BIS recommends a cap of €3,000 per household for digital euros. This limit allows citizens to enjoy the benefits of digital currency while preventing massive capital flight during crises. Interest rates on CBDCs must also be carefully calibrated-typically 0.5-1.0 percentage points below market rates-to avoid making them too attractive compared to bank products.

Operational Shifts: From Payments to Services

If CBDCs handle basic payments, what do banks do? They evolve. Traditional banks remain dominant in complex financial services like relationship-based lending, wealth management, and corporate finance. These areas require human judgment, risk assessment, and personalized service-things a digital ledger cannot replicate.

However, banks must adapt quickly. FTI Consulting notes that successful institutions are developing CBDC-compatible technologies and innovative financial products. Strategies include:

- Incentivizing Wallet Usage: Offering rewards for using CBDC wallets within the bank’s ecosystem.

- New Investment Products: Creating funds that leverage CBDC holdings for yield generation.

- Digital Credit Lines: Establishing instant credit facilities based on real-time CBDC transaction data.

The learning curve is steep. Full integration takes 18-24 months, requiring significant investment in blockchain expertise-a skill set currently scarce globally, with only 15,000 qualified professionals as of mid-2024. Banks that fail to upgrade face obsolescence, dropping from top-tier competitors to sixth place in long-term threat assessments.

Privacy Concerns and Public Trust

While efficiency gains are promising, privacy remains a major hurdle. CBDCs operate on digital ledgers that enable traceable records of all monetary movements. This transparency helps prevent money laundering and tax evasion but raises alarms about government surveillance.

User feedback from online communities reveals deep skepticism. In discussions on Reddit’s r/CBDC and r/Bitcoin, 78% of top posts mentioned privacy concerns, and 82% expressed doubt about government oversight. In the United States, 91% of commenters voiced reservations, compared to 67% in Europe. For CBDCs to succeed, central banks must design systems that balance anti-money laundering (AML) requirements with individual privacy rights. Technologies like zero-knowledge proofs may play a role here, allowing verification of transactions without revealing underlying details.

Global Competition and Monetary Sovereignty

CBDCs aren’t just changing domestic banking; they’re reshaping global power dynamics. Nations use digital currencies to assert monetary sovereignty, reducing reliance on foreign exchange systems dominated by the US dollar. The International Banker reports that CBDC adoption could reduce the dollar’s share of global reserves from 59% to 45% by 2035.

China’s digital yuan has reached 260 million users, demonstrating rapid scalability. Meanwhile, the European Central Bank targets a 2027 launch for the digital euro after successful interbank tests. The Reserve Bank of India expanded its digital rupee pilot to 15 cities, processing 5.7 million transactions by late 2024. As these systems mature, cross-border payments could become faster and cheaper, challenging legacy networks like SWIFT.

FAQ

Will CBDCs replace cryptocurrencies like Bitcoin?

No, CBDCs and cryptocurrencies serve different purposes. CBDCs are centralized, regulated, and backed by governments, aiming to modernize fiat currency. Cryptocurrencies like Bitcoin are decentralized, borderless, and often designed to operate outside traditional financial systems. They coexist rather than compete directly.

Are my CBDC funds safe if a bank fails?

Yes, CBDCs represent direct liabilities of the central bank, meaning they carry zero counterparty risk. Unlike bank deposits, which rely on insurance schemes, CBDC holdings are as safe as physical cash held by the state.

How will CBDCs affect small businesses?

Small businesses may benefit from faster, cheaper payments and improved access to credit through digital platforms. However, they could face challenges if banks reduce lending due to deposit outflows. Adaptation will depend on regulatory support and technological integration.

Can I use CBDCs anonymously?

Most CBDC designs prioritize traceability for security and compliance reasons. While some models allow limited anonymity for small transactions, large transfers typically require identity verification. Privacy protections vary by country and implementation strategy.

When will major economies launch CBDCs?

Timelines differ by region. China and the Bahamas have live systems. The EU aims for a 2027 launch of the digital euro. The US Federal Reserve continues research without a fixed date. India’s pilot program expands steadily, suggesting broader rollout within the next few years.

Filbert Reeves

June 23, 2026 AT 16:53oh great another article telling us how the government is gonna watch every penny we spend and call it 'safety' lol

like seriously do you people not read between the lines or are u just too busy worshipping at the altar of big tech? they want to kill cash because cash is untraceable. that's the whole point. if i can buy a coffee without the feds knowing my exact location and spending habits then they can't control me as effectively. but oh no, we need 'efficiency' and 'modernization'.

and don't get me started on this privacy nonsense with zero knowledge proofs. sounds like fancy computer speak for 'we still know everything about you but we won't tell anyone unless we feel like it.' classic. the fact that china already has this rolling out to millions of users should be a massive red flag for everyone here. they are building a social credit system in real time and calling it progress.

also why does nobody talk about what happens when the servers go down? or when they decide your account is frozen because you bought something they didn't like? traditional banks have flaws sure but at least there's some friction. with cbdc it's instant total control. scary stuff really.

Eric Scheinberg

June 23, 2026 AT 22:50The author presents a balanced overview of the structural shifts impending within the financial sector. It is imperative to recognize that disintermediation is not merely a theoretical risk but an operational reality that institutions must address proactively. The data regarding holding limits is particularly relevant for policy makers considering implementation strategies.

John Doe

June 25, 2026 AT 16:16I honestly feel for the bankers who have spent decades building relationships with clients only to see their core business model potentially dismantled by a few lines of code from a central bank. It’s terrifying to think about the human element being stripped away from finance completely. We are talking about livelihoods here not just abstract economic models. The anxiety in the industry is palpable and I think the public underestimates how much chaos this could cause if not managed with extreme care and empathy for those affected.

Skm Shubham

June 27, 2026 AT 00:03Typical western media spin trying to make surveillance state technology sound like a consumer benefit. You guys are so naive. Look at India we are moving fast because we understand that digital infrastructure is key for national security and economic dominance. The west is too bogged down in these silly privacy debates while we are actually getting things done. If you cannot adapt to the digital age you will be left behind. Stop complaining about tracking and start learning how to use the tools efficiently. Your hesitation is weakness.

Rob Aronson

June 27, 2026 AT 17:56From a fintech perspective the interoperability challenges are huge 🤔 Banks need to integrate CBDC wallets into existing core banking systems which is no small feat. The latency requirements for real-time gross settlement systems mean that legacy architectures will likely fail under stress tests. We are seeing a surge in demand for blockchain developers but the talent pool is still thin 📉. Institutions that don't pivot to API-first architectures now will struggle to offer the seamless UX customers expect. It’s a race against time and budget constraints are real 💸

Danna Charris

June 29, 2026 AT 09:12One must consider the implications for wealth management services. The affluent client base will undoubtedly seek alternative stores of value if CBDCs become the primary medium of exchange for retail transactions. Private banking will evolve significantly.

Fede Faith

June 29, 2026 AT 18:31Let's look at the practical side here. For small businesses faster payments mean better cash flow management which is crucial for survival. I've seen many shop owners struggle with delayed settlements from card processors. A CBDC could solve that instantly. However we need to ensure that the transition period doesn't leave older demographics behind. Training and support systems must be robust. It's not just about the tech it's about the people using it. We can guide this change positively if we focus on education and accessibility rather than fear.

Josh Dodson

July 1, 2026 AT 09:36i think its gonna be ok tho! lots of new jobs will pop up in cybersecurity and app dev. dont worry too much about it. the banks will figure it out eventually they always do. just keep ur money safe and learn how to use the new apps when they come out. its all part of the evolution right? 😊

Kumaran sowkarpet

July 2, 2026 AT 02:00In our region we have seen similar transitions with UPI and digital payments revolutionizing the economy. It brings financial inclusion to millions who were previously unbanked. The key is to maintain trust through transparency and user-centric design. We should share best practices globally to ensure that CBDCs serve the common good rather than just corporate interests. Let us work together to build a more inclusive financial future :)